Bits & Pieces

Edition #290 | 31/07/2026

Most traded | Markets & Macro | Earning Season | Honeywell | Chart of the Week | Energy ETFs | Product Spotlight | Scalable News | Retirement Spotlight

The word driving the market this week? CapEx. Recent earnings reports from the Magnificent 7 show the CapEx spending spree in full swing, with billions upon billions poured into AI. But throwing money at AI isn't cutting it anymore - investors now want to see those investments translate into real cash flow. Looming over all of this is the growing concern that the Fed might hike borrowing costs, which is hardly welcome news for capital-hungry tech giants. On a brighter note, Honeywell Technologies delivered some good news. And what was SpaceX again? Oh right, the ultimate IPO flop (so far).

Bought

Note: The data refers to the ratio of purchases and sales of the 100 most traded stocks in the Scalable broker between 24/07/2026 and 30/07/2026.

In the spotlight: Adidas

The World Cup drove Adidas to record Q2 revenue, powered by booming sportswear sales. But profits missed the mark, weighed down by heavy marketing spend that squeezed margins.

Strong earnings = even more hawkish Fed?

Kevin Warsh and the FOMC held rates steady on Wednesday at 3.5 % – 3.75 %. But market watchers sense a hawkish pivot and the writing is on the wall: inflation continues to run above the central bank’s 2% target, driven by high oil prices due to the escalation in the Strait of Hormuz. On top of that, the FOMC is split - for the first time since September 2016, three members dissented, voting in favor of an immediate 25-basis-point hike.

As a result, the CME FedWatch Tool now puts the odds of a 25 bps hike in September at 63.2%.

That looming rate hike is now casting a shadow over the US earnings season. While a whopping 85% of companies have beaten profit expectations - giving the Fed even more breathing room - rising rates mean valuation pressures are back. Richly valued tech stocks are taking the brunt of it. If you're pumping billions into AI, you need to deliver cash flow, and this earnings season is giving investors a look under the hood of the AI giants.

AI Impatience

Microsoft, Meta, Apple, and Amazon make up nearly a fifth of the S&P 500 by weight. But after AI hype fueled massive market rallies for months, investors are now taking a hard look at whether those multi-billion-dollar bets are actually paying off.

- Meta under pressure: Despite revenue jumping 28% year-over-year, Meta shares tumbled after-hours following its Q2 numbers. The issue? Soaring AI spending is chewing through cash, causing net income to shrink by 14%. Even so, the Instagram parent company bumped up its full-year AI investment guidance yet again.

- Microsoft delivers: Microsoft is also digging deep into its pockets for AI - except here, it’s already paying off. Fiscal year 2026 revenue (which wrapped up in June) surged 18% to $331 billion, driven by booming demand for AI and cloud services. The company expects double-digit growth and continued high investment for FY2027.

- Apple slides: Despite solid numbers, Apple slipped in late trading. While the iPhone maker boosted Q3 revenue by 16% on strong iPhone, Mac, and Services demand, China remains a persistent headwind. Revenue there rose 22.4%, falling $850 million short of Wall Street estimates. Guidance for the upcoming quarter was also disappointing.

- Amazon rides a cloud surge: The e-commerce titan logged its strongest quarterly cloud growth in over four years, pointing to heavy demand for AI. Amazon Web Services (AWS) jumped 37% to $42.2 billion - easily beating consensus estimates. CapEx is set to rise here as well.

A Major Transformation

Leaner and more specialized. That’s the path Honeywell has been carving out for a while now. After separating from its materials and quantum computing units, the legacy US conglomerate followed up in June by spinning off its iconic aviation division. Honeywell Aerospace is now a standalone public company. What remains operates as Honeywell Technologies - a focused, pure-play provider for industrial and building automation.

- Tech in high demand: With its automation solutions, Honeywell Technologies is positioned right at the intersection of several secular growth trends - including the AI boom, where it supplies control systems for data centers. It’s also tapping into decarbonization, offering power and climate controls for commercial real estate, one of the biggest drivers of carbon emissions.

- Earnings impress, guidance raised: Q2 revenue and EPS (excluding Honeywell Aerospace) beat Wall Street estimates across the board. Organic orders jumped 16% year-over-year, pushing its backlog to nearly $20 billion. Looking ahead, Honeywell Technologies now expects full-year 2026 organic revenue growth of 3% to 4%, up from its previous forecast of 2% to 3%.

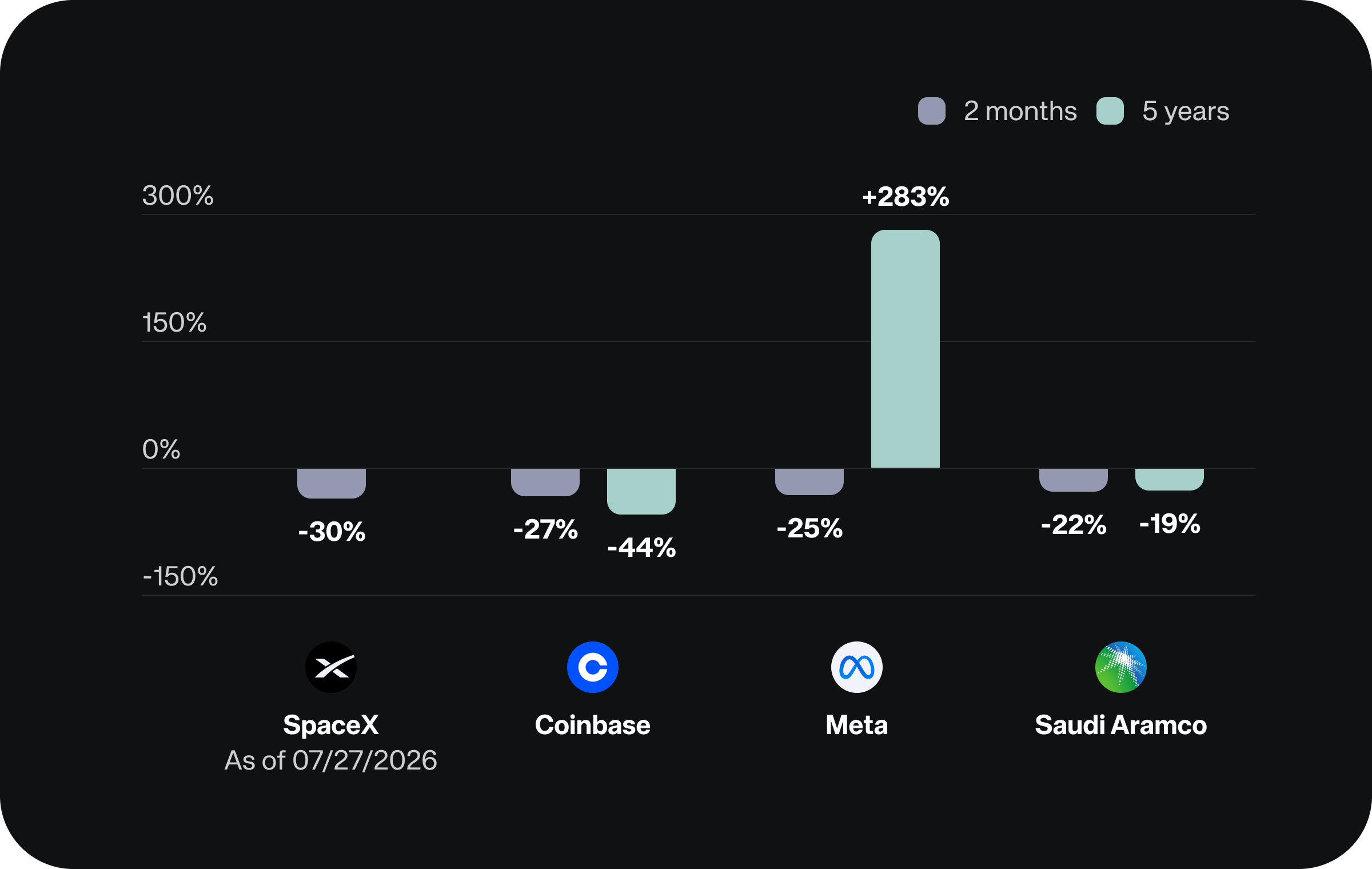

Overhyped and underdelivering? SpaceX ranks among top IPO flops

Share price performance post-debut

Source: Scalable internal research based on Yahoo Finance historical data.

It’s been almost two months since SpaceX made its rocket-fueled debut on Wall Street. But the astronomical highs from day one have fizzled out, with the stock sliding roughly 30% since. Measured by this post-IPO slump, SpaceX ranks among the weakest market debuts since the global financial crisis. So much for going "to the moon"?

Post-IPO pullbacks are nothing unusual, especially in tech. Grand growth narratives and good old-fashioned FOMO often push valuations to dizzying heights early on. Reality checks, profit-taking, and expiring lockup periods usually bring things back down to earth. Case in point: Meta dropped roughly 25% two months after its May 2012 debut, while both Saudi Aramco (Dec 2019) and Coinbase (April 2021) took heavy early hits as well. A rocky start doesn't dictate long-term performance, though - underlying fundamentals and broader macroeconomic conditions will ultimately steer the course.

Time to abandon the shuttle? While SpaceX’s fundamentals haven't quite lived up to expectations yet - its IPO valuation sat at a staggering 100x 2025 revenue - some analysts still see plenty of runway ahead. Potential index inclusions could also provide extra thrust, forcing ETF providers to buy up shares in bulk and putting a floor under the stock.

Powering Up Your Portfolio

Looking to big AI pioneers to drive portfolio returns? Not a bad play. But as earnings season is showing, expectations for tech giants are sky-high, and the market is punishing even the smallest missteps. For investors who still want a slice of the AI pie without all the tech volatility, the energy sector might be the sweet spot. Power-hungry data centers are driving massive revenue into energy coffers, with extra tailwinds coming from elevated oil prices and expanding grid infrastructure. A short-term trend? Hardly - electricity demand is set to surge even higher as AI and digitalization expand. The iShares MSCI World Energy Sector Advanced UCITS ETF offers easy, broad exposure to major traditional energy players like ExxonMobil, Chevron, and TotalEnergies. As a global energy export powerhouse, the US makes up roughly 60% of the fund’s weight.

A less US-heavy option: the Xtrackers MSCI Global SDG 7 Affordable and Clean Energy UCITS ETF 1C. This ETF focuses exclusively on companies driving clean energy transition. Another alternative would be the Amundi MSCI New Energy (Dist) targeting renewables, packing exposure to wind, solar, and next-gen clean tech.

Reaching for the Stars

Light-years away? Think again. Space starts just 100 kilometers above Earth's surface - and quietly powers our lives 24/7. Tracking a route on your phone, checking the weather, streaming live video, tapping to pay - without orbital tech, our modern world would grind to a halt in minutes. Anyone who thinks the "space economy" is strictly about rockets is missing an entire universe of opportunity.

According to a Morgan Stanley study, the space economy is projected to reach $1 trillion by 2040. Getting in on the action doesn't require playing stock picker with individual stars. With the newly launched iShares Space Technologies UCITS ETF, investors can add the entire cosmos to their portfolio in one move.

The lineup of underlying companies spans a wide galaxy: satellite network providers, data stream and drone specialists, chip and hardware makers, AI pioneers, and rocket manufacturers.

The fund benchmarks the STOXX Global Space Satellites and Drones Index, focusing heavily on industrial, tech, and communications equities. It holds over 80 companies across the globe (as of July 14, 2026), including Rocket Lab, Esco Technologies, and Korea Aerospace, with a Total Expense Ratio (TER) of 0.50%. The countdown is on.

Refer a friend

Investing is best done together. Refer Scalable to your family and friends and benefit from our tiered bonus of up to €200.

- 1st successful referral: €50 bonus

- 2nd successful referral: €100 bonus

- 3rd successful referral: €200 bonus

In this campaign, every new referral counts, regardless of how many people you have already referred. The terms and conditions apply.

In this section, we answer your most pressing questions on retirement planning in plain English.

Today’s Question: There’s a lot of buzz right now about the new "Early-Start Pension Act" (FrühStRG). What’s actually in the draft bill, and who stands to benefit?

On July 21, 2026, the Federal Ministry of Finance published the official draft bill (Referentenentwurf). The goal: to help kids and young adults start building wealth early through state-backed retirement savings. To kickstart this, the government is proposing a monthly allowance of €10 per child - adding up to a total of €1,440 in government funding per child over time.

- Who is it for? The initiative targets children and teenagers aged 6 to 17 who reside in Germany (transitional provisions apply).

- Where do things stand? This is designed as a state-subsidized retirement model, with the goal of making the benefits apply retroactively starting January 1, 2026.

- Good to know: It’s still early days. Because this is currently a draft bill, it still needs to go through votes in the Bundestag and Bundesrat, where details may still change.

As soon as the law is officially passed and the financial products are finalized, you’ll be the first to know right here!

Editorial deadline: Friday, 7 a.m.

Sources: Scalable and dpa-AFX