Emerging market equities: with or without China?

January 28, 2025 |

If you take the largest ETFs in Europe as an indicator of what ETF investors prefer to invest in, global and US ETFs are right at the top.1 What is sometimes forgotten about global share indices such as the MSCI World2 is the fact that shares from emerging markets are not represented there at all. Countries such as India, China, Brazil or Taiwan are not among the 23 industrialized countries included in the MSCI World Index, but are regarded as emerging economies.

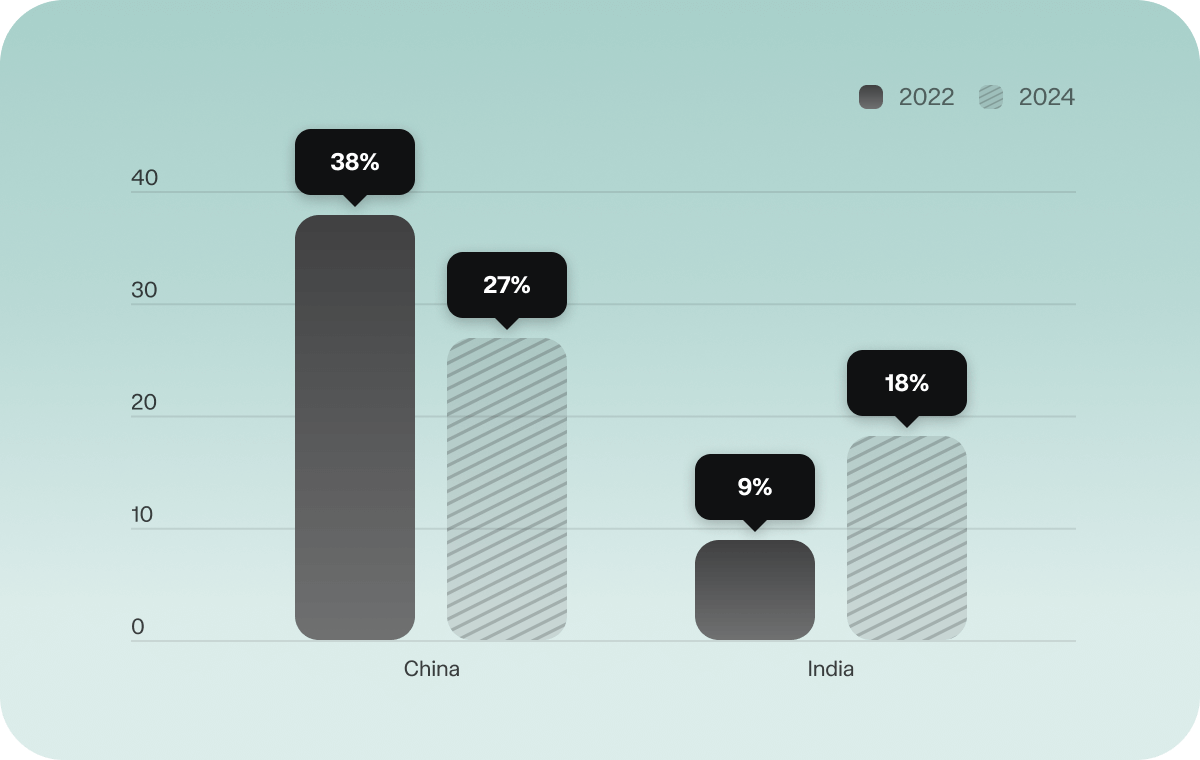

Emerging markets may have higher growth potential than developed regions, but they also have relevant risks. These include, for example, political uncertainty, geopolitical risks and possible economic or currency crises. The argument of diversification could be helpful for investors who are wondering whether they need emerging market equities in their portfolio at all. After all, the MSCI Emerging Markets index offers access to over 1,200 listed companies and therefore covers a large part of the emerging market equity market.3 The Chinese equity market has a special role to play here. Companies from China have accounted for a relatively high weighting in the MSCI Emerging Markets Index for a long time. In 2022, for example, the figure was 38%, which may have worried investors in view of the simmering trade conflict between China and the US. However, the index for emerging markets is changing.

Indian equities, which only accounted for 9% of the index a few years ago, are now challenging Chinese equities for first place. Today, China still has a weighting of around 27% in the MSCI Emerging Markets - significantly less than two years ago. Indian equities, on the other hand, now account for around 18% of the index, twice as much as just three years ago.4 Compared to the rest of the world, the Indian economy has enjoyed relatively high growth rates for years. These are also reflected to some extent in the Indian equity market, which has been able to achieve a higher weighting in emerging market ETFs over time. Investors in emerging market ETFs were therefore able to participate in India's growth story. Emerging countries are also constantly being added to the index. Countries such as the Czech Republic, Egypt or Indonesia were not even included in the index in 1998, but are now part of it.5

Weighting of India and China in the MSCI Emerging Markets Index

Source: DWS International GmbH, as of November 2024

As the Chinese equity market made up a large proportion of the MSCI Emerging Markets at times, emerging market ETFs that tracked an index variant without China6 became established on the market over time. Investors who want to reduce the China cluster risk can, for example, select an ETF based on the MSCI Emerging Markets ex-China index. The proportion of China in the portfolio can then be adjusted via a separate product, for example on the China index CSI 300.7

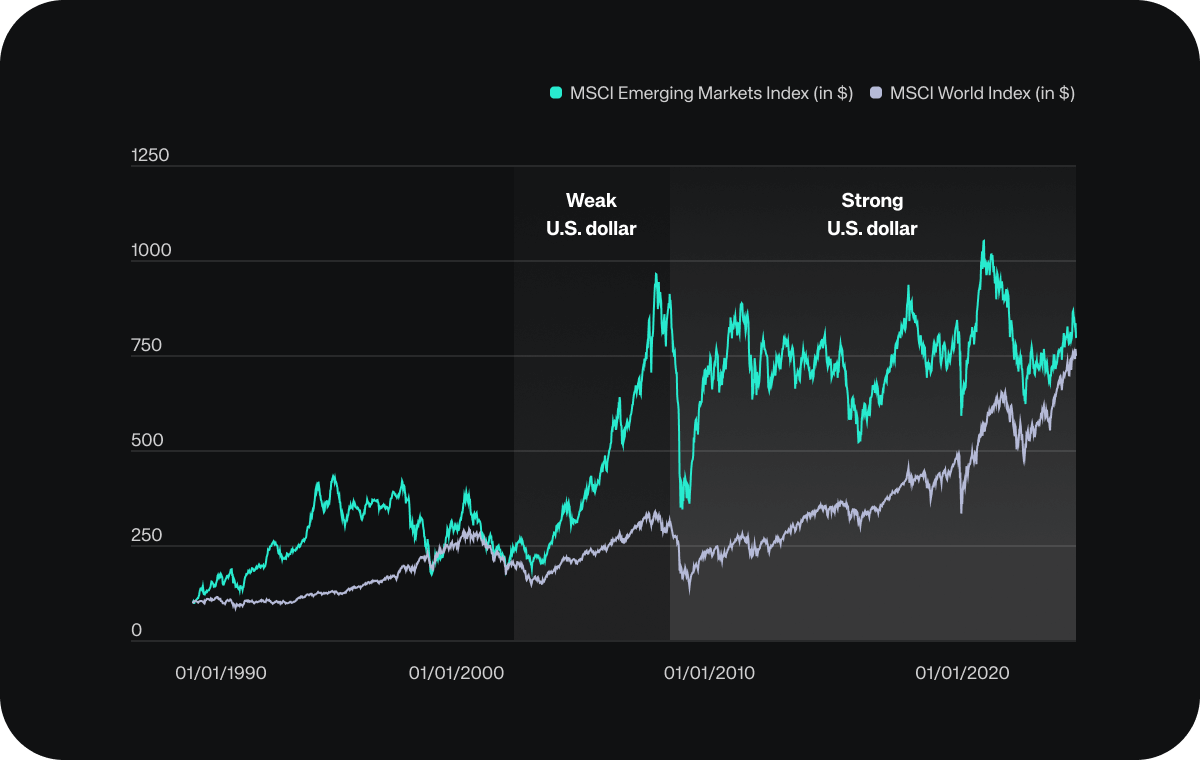

In the past, emerging market equities achieved returns that sometimes differed significantly from those of developed markets. The direction of the US dollar seemed to be a particularly relevant factor. Emerging market equities often performed better under a weak US dollar than under a strong US dollar. The following chart shows the historical performance of the MSCI World Index alongside the performance of the MSCI Emerging Markets Index. The area highlighted in green marks a phase in which the US currency weakened. The red background indicates a period in which the US dollar tended to strengthen.8

Source: DWS International GmbH, as of November 2024

In addition, the emerging markets have historically benefited from the US Federal Reserve Bank (Fed) lowering its key interest rate. The markets are currently assuming that the Fed will cut its key interest rate further next year. This is a possible factor that could provide a tailwind for emerging market equities in 2025. While shares in developed countries could come under pressure in the event of a weak US dollar.

Important notes

This document is a marketing communication document.

All statements of opinion reflect the current assessment, which may change without prior notice. Forecasts are based on assumptions, estimates, opinions and hypothetical models or analyses that may prove to be incorrect or inaccurate. Past performance is not a reliable indicator of future performance. Source: DWS International GmbH; as of Dec 4, 2024

1 justetf.de // MSCI EM in fifth place, right after US/Global.

2 The MSCI World is a global share index that tracks the performance of around 1,500 shares from 23 industrialized countries.

3 Source: https://www.msci.com/documents/10199/c0db0a48-01f2-4ba9-ad01-226fd5678111

4 Source: https://en.guidingdata.com/msci-em-top-10-constituents-development/

5 Source: https://www.msci.com/indexes/group/emerging-markets-indexes

6 The MSCI Emerging Markets ex China Index provides access to the largest and most liquid stocks from emerging markets excluding China.

7 The CSI 300 (China Securities Index 300) is a share index that tracks the performance of the two largest stock exchanges in mainland China, Shanghai and Shenzhen.

8 Source: Bloomberg, presentation by DWS. Data is based on price indices, as these have a longer history than the MSCI Emerging Markets Net Total Return Index. Dividends were therefore not taken into account. The US Dollar Index (DXY Index) was used as an indicator of the strength or weakness of the US Dollar.

Risk Disclaimer – There are risks associated with investing. The value of your investment may fall or rise. Losses of the capital invested may occur. Past performance, simulations or forecasts are not a reliable indicator of future performance. We do not provide investment, legal and/or tax advice. Should this website contain information on the capital market, financial instruments and/or other topics relevant to investment, this information is intended solely as a general explanation of the investment services provided by companies in our group. Please also read our risk information and terms of use.